Cargo insurance is shipment coverage that helps shippers recover losses when freight is damaged, stolen, or lost in transit. Unlike carrier liability, which may be limited by law or contract, a cargo policy can provide broader protection based on the purchased limits, exclusions, and claim terms. Insuring your cargo protects your business’s bottom line, and shippers who rely strictly on carrier liability as defined in The Carmack Amendment (49 U.S.C. § 14706) when shipping across state lines could be compensated for just pennies on the dollar of the value of their shipment.

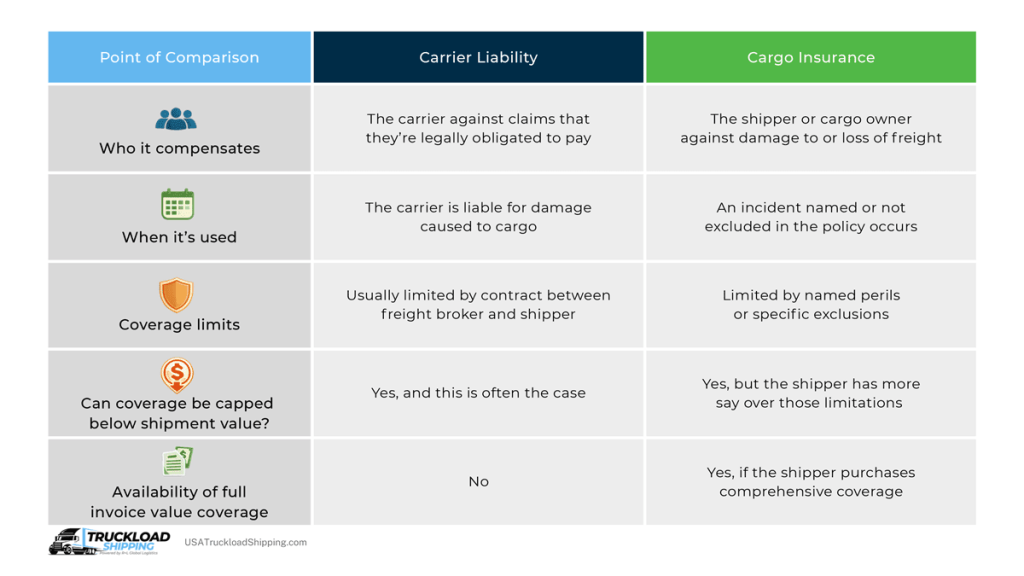

Carrier liability is the carrier’s legal responsibility for freight loss or damage while the shipment is in its care. Cargo insurance is separate protection purchased to cover the shipper’s financial loss, often with broader reimbursement options and clearer claim pathways.

In the following table, I’ve laid out some of the most notable differences between cargo insurance and carrier liability.

Carriers and freight brokers usually limit the amount of money they pay out for liability claims in contracts and arrangements with their clients (shippers).

Example: A shipper moves $85,000 of branded consumer electronics via LTL in winter. Carrier liability may not reimburse full invoice value if the contract caps exposure. A separate policy can cover theft or damage based on purchased limits and exclusions.

Carrier liability covers freight damages and loss resulting from the following scenarios:

This list is not comprehensive, but includes some of the most common scenarios that trigger carrier liability.

Coverage gaps under The Carmack Amendment can be expressed by the following five legal defenses:

Cargo insurance policies can be tailored to account for these defenses, which carrier liability doesn’t cover.

When you purchase cargo insurance for your shipment, you should confirm the following details on the policy and make adjustments if required:

I’ll examine these in greater detail in the sections below.

Cargo insurance limits are provisions in the policy that establish scenarios under which the policyholder will not receive compensation for lost or damaged cargo. Insurance policies for cargo can be largely grouped into two different types:

Cargo insurance limits define the maximum amount the policy can pay for a covered loss. Those limits may be based on invoice value, declared value, replacement cost, or other policy terms.

Exclusions to cargo insurance are, as previously implied, enumerated in all-risk policies to limit circumstances under which compensation would be provided to the policyholder. An otherwise all-risk policy could be tailored to exclude situations such as:

When purchasing a cargo insurance policy, you should consider factors that increase chances of cargo damage. For instance, if you’re shipping freight during the winter months, make sure your policy doesn’t exclude freeze damage, weather-related delays, or temperature-related spoilage where relevant.

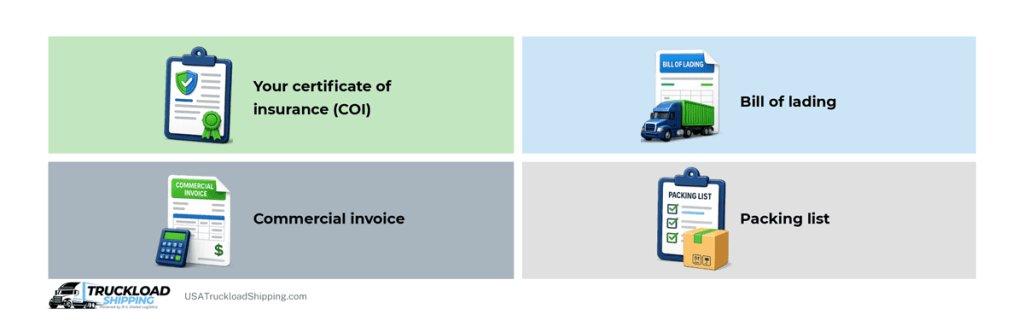

Cargo insurance claims must be made within time windows specified in the insurance policy. The shipper will also need to have the following documents pertaining to the affected shipment available when submitting a cargo insurance claim:

You may require additional documents depending on factors like the type of commodity you were shipping, but any cargo insurance policy will specify what those requirements are should you need to make a claim.

Choose a cargo insurance policy based on the value of the shipment, the type of goods, the route risk, and the policy exclusions. The right policy should cover your likely loss scenarios, not just offer the lowest premium.

Before buying, confirm:

A good policy is one that matches your shipment’s actual risk and gives you a realistic path to full reimbursement if something goes wrong.

Shippers should consider added coverage when shipment value, theft exposure, handling complexity, weather risk, or claims urgency exceeds what standard carrier liability is likely to reimburse. This is especially true for electronics, food, branded goods, and multi-stop or LTL freight.

Some common scenarios in which shippers should strongly consider purchasing additional coverage include:

The cost of cargo insurance coverage pales in comparison to the cost of replacing uninsured goods should a worst-case scenario occur.

When you ship your goods with USA Truckload Shipping, you have the option of insuring the cargo. The peace of mind that comes with knowing your shipment is covered is often worth the investment. Call our team of freight shipping experts at (866) 353-7178 or get a quote online in just minutes.

Does carrier liability automatically cover the full value of my shipment?

Usually not. Liability is often limited by the carrier’s contract with the shipper.

What does cargo insurance typically cover?

Cargo insurance is generally used to protect against freight that is lost, damaged, or stolen in transit.

Can I buy cargo insurance through a freight broker or shipping provider?

Yes, we offer cargo insurance options for shippers who choose to let us handle their freight shipping needs.

Works Cited:

49 U.S. Code 14706 - Liability of Carriers Under Receipts and Bills of Lading, Legal Information Institute, Cornell Law School

You Are Presumed Liable, eTrucker, Seaton, Henry E., 2005

Inherent Vice, North Standard, 2017

Acts of the Public Enemy Clause Samples, Law Insider

Insurance Exclusions Explained, Thimble

R+L Global Logistics

315 NE 14th St., Ocala, FL 34470